The Compliance Gap Between Third Party NIL and Revenue Sharing

How NIL Go and CAPS apply different standards to athlete NIL compensation

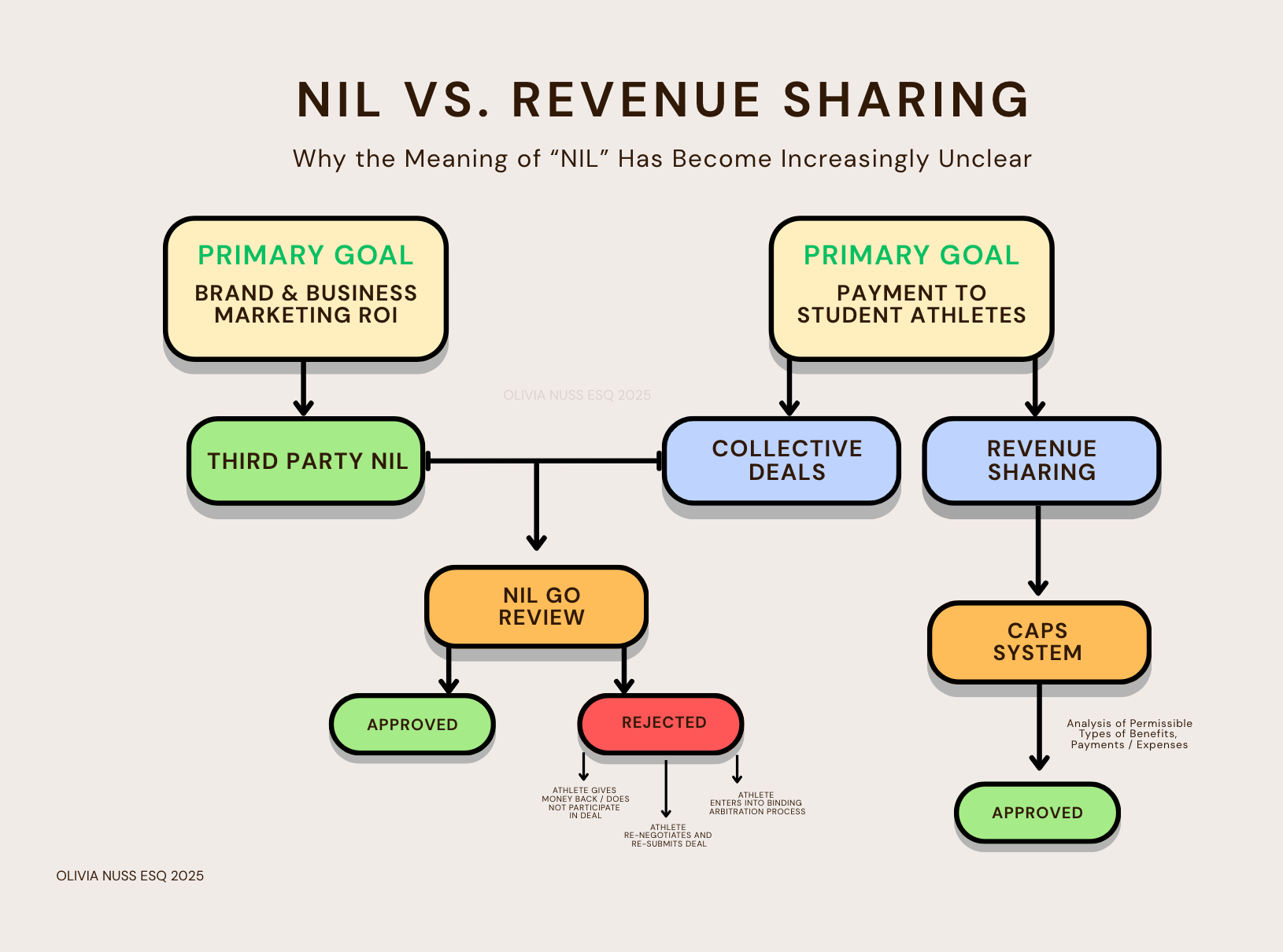

In my last article, How NIL Go Regulates Third Party NIL Deals for College Athletes, I begin to explore how the compliance ecosystem is structured around third-party NIL deals between athletes and external sponsors, companies, entities, or brands. These agreements are submitted into NIL Go, where they are reviewed under specific CSC standards, including:

Valid business purpose

Fair market value compensation

Range of compensation (relative to similarly situated individuals and services rendered)

This review framework is very intentionally designed to filter out pay-for-play structures, impermissible recruiting inducements, or inflated valuations without a real commercial basis. The CSC, with Deloitte’s assistance, evaluates reported agreements against those criteria and can clear, reject, or flag deals for further review or arbitration based on a failure to meet them.

I also recently wrote NIL vs. Revenue Sharing: Two Systems, One Vocabulary, which explains how revenue-sharing deals (arrangements where institutions distribute portions of athletic program income back to students) are fundamentally a different economic construct, distinct from true “market-based” NIL compensation, even if they are sometimes labeled or processed similarly to NIL in practice.

The Core Issue: Different Evaluation Standards

The central tension is this: third-party NIL deals are reviewed for valid business purpose, fair value, and whether compensation falls within a reasonable range, while school-funded revenue-sharing under CAPS faces no comparable substantive review.

Under the House v. NCAA settlement, the College Sports Commission (CSC) oversees both third-party NIL agreements and school-funded revenue-sharing payments. Third-party NIL deals are submitted through NIL Go and evaluated before an athlete can accept them. Revenue-sharing payments, by contrast, are reported through the College Athlete Payment System (CAPS), which primarily tracks distributions to ensure schools remain within the annual cap.

That creates a governance gap. The CSC applies a market-based valuation review to third-party NIL deals, but CAPS does not appear to require a parallel evaluation of revenue-sharing allocations. There is no explicit requirement that revenue-sharing payments reflect fair market value, a defined commercial purpose, or meaningful services rendered.

Let’s put this in plain english:

Third-party NIL deals have to prove they’re legit. There needs to be a real business reason for the payment, and the amount has to look like something you’d actually see in the NIL market. NIL Go checks that before the athlete can get paid.

Revenue-sharing is different. Under CAPS, the main question is basically: does the school stay under the $20.5M cap?If it does, the payment goes through, without the same kind of “is this deal real and fairly priced?” review.

This creates a clear discrepancy in how “NIL-related” compensation is evaluated, based on the source of funds.

Why This Matters

Right now, the system applies two very different standards to payments that are often described using the same “NIL” vocabulary. Third-party NIL deals must clear a substantive market review before an athlete can be paid. Revenue-sharing payments, however, can be approved with little more than a cap check. That mismatch isn’t just technical; it shapes how money moves through college sports and what kinds of payments regulators effectively allow.

The practical consequence is predictable: compensation that would trigger scrutiny in the NIL Go system could be replicated through revenue sharing (deals directly from the university) without any comparable valuation or purpose-based review. That creates inconsistent enforcement, invites workarounds, and weakens trust in the regulatory framework.

Is Revenue-Sharing NIL?

If the goal is integrity and transparency in NIL compensation, the rules should either apply comparable substantive guardrails to revenue sharing or clearly define revenue sharing as a distinct category of payment, regulated differently by design.

Otherwise, we should be honest about what it is: revenue sharing is a separate compensation model, not NIL.

The information provided in this article is for general informational purposes only and is not intended as legal advice. Readers should consult their own legal or compliance advisors regarding specific circumstances.